Exam 15: Estimation of Dynamic Causal Effects

Exam 1: Economic Questions and Data17 Questions

Exam 2: Review of Probability71 Questions

Exam 3: Review of Statistics63 Questions

Exam 4: Linear Regression With One Regressor65 Questions

Exam 5: Regression With a Single Regressor: Hypothesis Tests and Confidence Intervals59 Questions

Exam 6: Linear Regression With Multiple Regressors65 Questions

Exam 7: Hypothesis Tests and Confidence Intervals in Multiple Regression65 Questions

Exam 8: Nonlinear Regression Functions62 Questions

Exam 9: Assessing Studies Based on Multiple Regression65 Questions

Exam 10: Regression With Panel Data50 Questions

Exam 11: Regression With a Binary Dependent Variable50 Questions

Exam 12: Instrumental Variables Regression50 Questions

Exam 13: Experiments and Quasi-Experiments50 Questions

Exam 14: Introduction to Time Series Regression and Forecasting50 Questions

Exam 15: Estimation of Dynamic Causal Effects50 Questions

Exam 16: Additional Topics in Time Series Regression50 Questions

Exam 17: The Theory of Linear Regression With One Regressor49 Questions

Exam 18: The Theory of Multiple Regression50 Questions

Select questions type

You are hired to forecast the unemployment rate in a geographical area that is peripheral to a large metropolitan area in the United States.The area in question is called the Inland Empire (San Bernardino County and Riverside County)and is situated east of Greater Los Angeles (Los Angeles County and Orange County).While the area has a large population (it is the 14th largest metropolitan statistical area in the United States),its economic activity relies heavily on that of the larger area it is attached to.For example,it is estimated that approximately 20% of its workforce commutes into the Greater Los Angeles area for work and few workers commute the other way.Furthermore,its logistics industry is heavily dependent on economic activity in the Greater Los Angeles Area.As a result,you view the unemployment rate of the Greater Los Angeles Area (urGLA)to be exogenous in determining the unemployment rate in the Inland Empire (urIE).You estimate the following distributed lag model,where numbers in parenthesis are HAC standard errors:

Δ  = 0.00002 + 0.74 Δ

= 0.00002 + 0.74 Δ  - 0.04 Δ

- 0.04 Δ  - 0.01 Δ

- 0.01 Δ  + 0.07 Δ

+ 0.07 Δ  + 0.05 Δ

+ 0.05 Δ  (0.00010)(0.06)(0.06)(0.06)(0.06)(0.06)

+ 0.09 Δ

(0.00010)(0.06)(0.06)(0.06)(0.06)(0.06)

+ 0.09 Δ  + 0.10Δ

+ 0.10Δ  (0.05)(0.06)

t = 1991:01-2009:12,R2 = 0.60,SER = 0.001

a.What is the impact effect of a one percentage point increase (say from 0.06 to 0.07)of the unemployment rate in the Greater Los Angeles area?

b.What is the long-run cumulative dynamic multiplier?

c.Why do you think the variables above appear in changes rather than in levels?

(0.05)(0.06)

t = 1991:01-2009:12,R2 = 0.60,SER = 0.001

a.What is the impact effect of a one percentage point increase (say from 0.06 to 0.07)of the unemployment rate in the Greater Los Angeles area?

b.What is the long-run cumulative dynamic multiplier?

c.Why do you think the variables above appear in changes rather than in levels?

(Essay)

4.7/5  (43)

(43)

The Gallup Poll frequently surveys the electorate to quantify the public's opinion of the president.Since 1945,Gallup settled on the following wording of its presidential poll: "Do you approve or disapprove of the way (name)is handling his job as president?" Gallup has not changed its presidential question since then,and respondents can answer "approve," "disapprove," or "no opinion."

You want to see how this approval rating is related to the Michigan index of consumer sentiment (ICS).The monthly survey,conducted with a minimum sample of 500,asks people if they feel "better/worse off" with regard to current and future conditions.

(a)To estimate dynamic causal effects,you collect quarterly data from 1962:I - 1998:II for the United States.You allow a binary variable for each presidency to capture the intrinsic popularity of the President.Furthermore,you eliminate observations that include a change in party for the presidency by using a binary variable,which takes on the value of one during the first quarter of the year after the election.Finally,a friendly political scientist provides you with (i)an "events" variable, (ii)a "Vietnam" binary variable,and (iii)a "honeymoon" variable,which measures the effect of a higher popularity of a president immediately following the election.(The coefficients of these variables will not be reported here. )

Assuming that consumer sentiment is exogenous,you estimate the following two specifications (numbers in parenthesis are heteroskedasticity- and autocorrelation-consistent standard errors):  t = 26.08 + 0.178 × ICSt + 0.232 × ICSt-1;R2= 0.667,SER = 7.00

(8.83)(0.120)(0.135)

t = 26.08 + 0.178 × ICSt + 0.232 × ICSt-1;R2= 0.667,SER = 7.00

(8.83)(0.120)(0.135)  t = 26.08 + 0.178 × ΔICSt + 0.411 + ICSt-1;R2 = 0.667,SER = 7.00

(8.17)(0.120 )(0.089)

What is the difference between the two specifications? What is the advantage of estimating the second equation,if any?

(b)Assuming that the errors follow an AR(1)process,you also estimate the following alternative:

t = 26.08 + 0.178 × ΔICSt + 0.411 + ICSt-1;R2 = 0.667,SER = 7.00

(8.17)(0.120 )(0.089)

What is the difference between the two specifications? What is the advantage of estimating the second equation,if any?

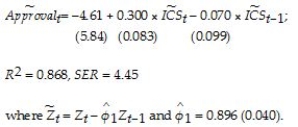

(b)Assuming that the errors follow an AR(1)process,you also estimate the following alternative:  t = -4.61 + 0.300 × ICSt - 0.070 × ICSt-1- 0.054 × ICSt-2;+ 0.776 × Approvalt-1;

(5.84)(0.083)(0.099)(0.083)(0.057)

R2 = 0.868,SER = 4.45

How is this specification related to the previous ones? What implicit assumptions did you have to make to allow for desirable properties of the OLS estimator?

(c)You finally estimate the approval equation using the quasi-difference specification and the GLS estimator.

t = -4.61 + 0.300 × ICSt - 0.070 × ICSt-1- 0.054 × ICSt-2;+ 0.776 × Approvalt-1;

(5.84)(0.083)(0.099)(0.083)(0.057)

R2 = 0.868,SER = 4.45

How is this specification related to the previous ones? What implicit assumptions did you have to make to allow for desirable properties of the OLS estimator?

(c)You finally estimate the approval equation using the quasi-difference specification and the GLS estimator.  How is this equation related to the ones in (a)and (b)? What are the properties of the GLS estimator here,under the assumption that ICS is strictly exogenous?

(d)Is it likely that the ICS is exogenous here? Strictly exogenous?

How is this equation related to the ones in (a)and (b)? What are the properties of the GLS estimator here,under the assumption that ICS is strictly exogenous?

(d)Is it likely that the ICS is exogenous here? Strictly exogenous?

(Essay)

4.8/5 (37)

In your intermediate macroeconomics course,government expenditures and the money supply were treated as exogenous,in the sense that the variables could be changed to conduct economic policy to influence target variables,but that these variables would not react to changes in the economy as a result of some fixed rule.The St.Louis Model,proposed by two researchers at the Federal Reserve in St.Louis,used this idea to test whether monetary policy or fiscal policy was more effective in influencing output behavior.Although there were various versions of this model,the basic specification was of the following type:

Δln(Yt)= β0 + β1Δln mt + ...+ βpΔln mt-p-1 + βp+1Δln Gt + ...+ βp+qΔln Gt-q-1 + ut

Assuming that money supply and government expenditures are exogenous,how would you estimate dynamic causal effects? Why do you think this type of model is no longer used by most to calculate fiscal and monetary multipliers?

(Essay)

4.9/5 (32)

The distributed lag model assumptions include all of the following with the exception of:

(Multiple Choice)

4.9/5 (29)

Your textbook mentions heteroskedasticity- and autocorrelation- consistent standard errors.Explain why you should use this option in your regression package when estimating the distributed lag regression model.What are the properties of the OLS estimator in the presence of heteroskedasticity and autocorrelation in the error terms? Explain why it is likely to find autocorrelation in time series data.If the errors are autocorrelated,then why not simply adjust for autocorrelation by using some non-linear estimation method such as Cochrane-Orcutt?

(Essay)

4.8/5 (39)

(Requires some calculus)In the following,assume that Xt is strictly exogenous and that economic theory suggests that,in equilibrium,the following relationship holds between Y* and Xt,where the "*" indicates equilibrium.

Y* = kXt

An error term could be added here by assuming that even in equilibrium,random variations from strict proportionality might occur.Next let there be adjustment costs when changing Y,e.g.costs associated with changes in employment for firms.As a result,an entity might be faced with two types of costs: being out of equilibrium and the adjustment cost.Assume that these costs can be modeled by the following quadratic loss function:

L = λ1(Yt - Y*)2 + λ1(Yt - Yt-1)2

a.Minimize the loss function w.r.t.the only variable that is under the entity's control,Yt and solve for Yt.

b.Note that the two weights on Y* and Yt-1 add up to one.To simplify notation,let the first weight be θ and the second weight (1-θ).Substitute the original expression for Y* into this equation.In terms of the ADL(p,q)terminology,what are the values for p and q in this model?

(Essay)

4.8/5 (34)

Consider the following model Yt = β0 +  + ut where the superscript "e" indicates expected values.This may represent an example where consumption depends on expected,or "permanent," income.Furthermore,let expected income be formed as follows:

+ ut where the superscript "e" indicates expected values.This may represent an example where consumption depends on expected,or "permanent," income.Furthermore,let expected income be formed as follows:  =

=  + λ(Xt -

+ λ(Xt -  );0 < λ < 1

(a)In the above expectation formation hypothesis,expectations are formed at the end of the period,say the 31st of December,if you had annual data.Give an intuitive explanation for this process.

(b)Rewrite the expectations equation in the following form:

);0 < λ < 1

(a)In the above expectation formation hypothesis,expectations are formed at the end of the period,say the 31st of December,if you had annual data.Give an intuitive explanation for this process.

(b)Rewrite the expectations equation in the following form:  = (1 - λ)

= (1 - λ)  + λXt

Next,following the method used in your textbook,lag both sides of the equation and replace

+ λXt

Next,following the method used in your textbook,lag both sides of the equation and replace  .Repeat this process by repeatedly substituting expression for

.Repeat this process by repeatedly substituting expression for  ,

,  ,and so forth.Show that this results in the following equation:

,and so forth.Show that this results in the following equation:  = λXt + λ(1-λ)Xt-1 + λ(1- λ)2 Xt-2 + ...+ λ(1- λ)n Xt-n + (1 - λ)n+1

= λXt + λ(1-λ)Xt-1 + λ(1- λ)2 Xt-2 + ...+ λ(1- λ)n Xt-n + (1 - λ)n+1  Explain why it is reasonable to drop the last right hand side term as n becomes large.

(c)Substitute the above expression into the original model that related Y to

Explain why it is reasonable to drop the last right hand side term as n becomes large.

(c)Substitute the above expression into the original model that related Y to  .Although you now have right hand side variables that are all observable,what do you perceive as a potential problem here if you wanted to estimate this distributed lag model without further restrictions?

(d)Lag both sides of the equation,multiply through by (1- λ),and subtract this equation from the equation found in (c).This is called a "Koyck transformation." What does the resulting equation look like? What is the error process? What is the impact effect (zero-period dynamic multiplier)of a unit change in X,and how does it differ from long run cumulative dynamic multiplier?

.Although you now have right hand side variables that are all observable,what do you perceive as a potential problem here if you wanted to estimate this distributed lag model without further restrictions?

(d)Lag both sides of the equation,multiply through by (1- λ),and subtract this equation from the equation found in (c).This is called a "Koyck transformation." What does the resulting equation look like? What is the error process? What is the impact effect (zero-period dynamic multiplier)of a unit change in X,and how does it differ from long run cumulative dynamic multiplier?

(Essay)

4.8/5 (35)

Consider the distributed lag model Yt = β0 + β1Xt + β2Xt-1 + β3Xt-2 + … + βr+1Xt-r + ut.The dynamic causal effect is

(Multiple Choice)

4.8/5 (42)

In the distributed lag model,the coefficient on the contemporaneous value of the regressor is called the

(Multiple Choice)

4.9/5 (44)

It has been argued that Canada's aggregate output growth and unemployment rates are very sensitive to United States economic fluctuations,while the opposite is not true.

(a)A researcher uses a distributed lag model to estimate dynamic causal effects of U.S.economic activity on Canada.The results (HAC standard errors in parenthesis)for the sample period 1961:I-1995:IV are:  t = -1.42 + 0.717 × urust + 0.262 × urust-1 + 0.023 × urust-2 - 0.083 × urust-3

(0.83)(0.457)(0.557)(0.398)(0.405)

- 0.726 × urust-4 + 1.267 × urust-5;R2= 0.672,SER = 1.444

(0.504)(0.385)

where urcan is the Canadian unemployment rate,and urus is the United States unemployment rate.

Calculate the long-run cumulative dynamic multiplier.

(b)What are some of the omitted variables that could cause autocorrelation in the error terms? Are these omitted variables likely to uncorrelated with current and lagged values of the U.S.unemployment rate? Do you think that the U.S.unemployment rate is exogenous in this distributed lag regression?

t = -1.42 + 0.717 × urust + 0.262 × urust-1 + 0.023 × urust-2 - 0.083 × urust-3

(0.83)(0.457)(0.557)(0.398)(0.405)

- 0.726 × urust-4 + 1.267 × urust-5;R2= 0.672,SER = 1.444

(0.504)(0.385)

where urcan is the Canadian unemployment rate,and urus is the United States unemployment rate.

Calculate the long-run cumulative dynamic multiplier.

(b)What are some of the omitted variables that could cause autocorrelation in the error terms? Are these omitted variables likely to uncorrelated with current and lagged values of the U.S.unemployment rate? Do you think that the U.S.unemployment rate is exogenous in this distributed lag regression?

(Essay)

4.8/5 (36)

Your textbook presents as an example of a distributed lag regression the effect of the weather on the price of orange juice.The authors mention U.S.income and Australian exports,oil prices and inflation,monetary policy and inflation,and the Phillips curve as other potential candidates for distributed lag regression.You are considering estimating the effect of minimum wages on teenage employment (employment population ratio)using a time series of U.S.data.Write a short essay on whether a distributed lag model would be a suitable tool to figure out dynamic causal effects in this case.

(Essay)

4.8/5 (38)

(Requires Appendix material)Your textbook states that in "the distributed lag regression model,the error term ut can be correlated with its lagged values.This autocorrelation arises,because,in time series data,the omitted factors that comprise ut can themselves be serially correlated."

(a)Give an example what the authors have in mind.

(b)Consider the ADL model,where the X's are strictly exogenous,and there is no autocorrelation (and/or heteroskedasticity)in the error term.  (d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(Essay)

4.9/5 (42)

Heteroskedasticity- and autocorrelation-consistent standard errors

(Multiple Choice)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)